In the North Carolina High Country, your closing costs aren’t just administrative fees; they’re a strategic investment in your mountain legacy. You’ve likely felt the weight of uncertainty when evaluating luxury estates or expansive acreage, wondering how the state’s unique “Due Diligence” system impacts your liquid capital. It’s natural to feel anxious about hidden fees or the specialized inspection costs required for high-elevation properties. Understanding the nuances of closing costs in North Carolina is the first step toward a confident, seamless transaction.

We agree that transparency is paramount when you’re securing a high-stakes investment. This expert breakdown empowers you to master the complexities of the 2026 market, ensuring you can budget with precision for your next mountain retreat. You’ll receive a detailed look at the essential line items you’ll encounter, such as the $2.00 per $1,000 excise tax and the favorable property tax rates in Watauga, Ashe, and Avery counties. We’ll also clarify the state’s attorney-led closing requirements and the critical distinction between non-refundable due diligence fees and your earnest money deposit.

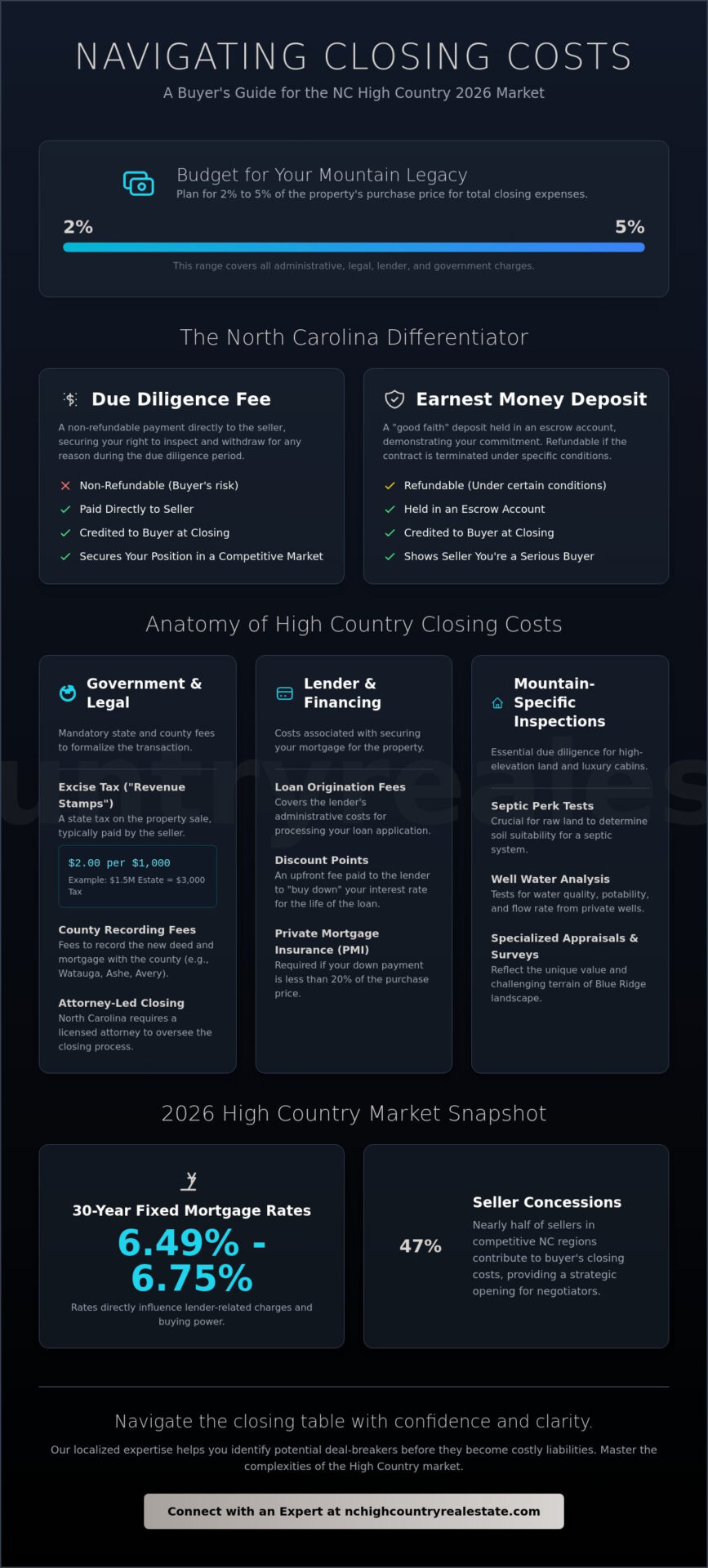

Key Takeaways

- Learn why the North Carolina Due Diligence fee is non-refundable and how it strategically secures your position in a competitive mountain market.

- Gain a clear line-item understanding of closing costs in North Carolina, including the $2.00 per $1,000 excise tax and specific recording fees for 2026.

- Identify the specialized “Mountain Tax” inspection costs essential for luxury cabins and high-elevation land, from septic perk tests to well water analysis.

- Discover how to accurately budget between 2% and 5% of your purchase price to ensure a smooth transition into your new mountain estate.

- Understand how localized expertise helps you identify potential “deal-breakers” before they become costly liabilities at the closing table.

Understanding Closing Costs in North Carolina: An Overview for 2026

The final hurdle in your journey to mountain homeownership isn’t the steep incline of a Blue Ridge driveway; it’s the settlement table. Understanding Closing Costs is essential for any buyer looking to secure a legacy property in the High Country. These fees represent the various administrative, legal, and government charges required to finalize your real estate transaction. While the numbers can seem daunting, North Carolina remains one of the more cost-effective states for real estate closings. This efficiency is largely due to our streamlined attorney-led process, which keeps high-stakes transactions organized and transparent.

It’s vital to distinguish between your out-of-pocket expenses and your at-table settlement costs. Pre-closing expenses, such as your non-refundable due diligence fee and specialized mountain inspections, are paid early in the process. Settlement costs are the fees listed on your final disclosure that you’ll pay when you sign the deed. By separating these in your mind, you can maintain a clearer picture of your liquidity throughout the purchase of a luxury estate or expansive acreage.

The 2026 High Country Market Context

Current market dynamics are shifting how we approach these fees. As of May 2026, 30-year fixed mortgage rates are hovering between 6.49% and 6.75%. These rates directly influence lender-related charges, such as origination fees and discount points. In luxury markets like Boone and Blowing Rock, transactions require more rigorous financial preparation. Sellers are increasingly offering concessions, with nearly 47% of recent resale closings in competitive NC regions including some form of seller contribution to the buyer’s closing costs in North Carolina. This trend provides a strategic opening for savvy negotiators to offset their initial investment.

Estimating Your Total Investment

Most buyers should budget between 2% and 5% of the property’s purchase price for their total closing expenses. For a median-priced home in the state, which sits around $382,211, this translates to a manageable range. However, land acquisitions in Ashe County often carry higher fixed costs relative to the purchase price. Items like perk tests and septic inspections are non-negotiable for raw land. You’ll receive a Loan Estimate shortly after your application and a Closing Disclosure three days before settlement. These documents are your roadmap. They ensure there are no surprises when you finally reach the summit of your real estate journey and secure your piece of the High Country.

The Anatomy of NC Closing Fees: A Detailed Breakdown

Moving from a broad estimate to a line-item budget requires a surgical look at where your capital goes during a High Country transaction. While the total closing costs in North Carolina typically range from 2% to 5% of the purchase price, the specific distribution of these funds varies significantly for luxury mountain estates. High-elevation properties often demand more complex surveys and specialized appraisals that reflect the unique value of the Blue Ridge landscape. For those exploring entry-level options or seeking grants, resources for North Carolina closing cost assistance can provide a helpful starting point, though luxury buyers usually focus on optimizing their private financing structures.

Lender and Financing Charges

Lender fees are the most variable component of your settlement statement. In 2026, with mortgage rates between 6.49% and 6.75%, many buyers choose to pay discount points at closing. This upfront fee effectively “buys down” your interest rate, which can save thousands over the life of a loan on a multi-million dollar mountain home. You’ll also encounter loan origination fees, which cover the administrative costs of processing your file. If your down payment is less than 20%, remember to account for private mortgage insurance (PMI) premiums. These are often required as an initial escrow deposit at the closing table.

Title, Tax, and Legal Protections

North Carolina’s tax structure is transparent but requires precise calculation. The state levies an Excise Tax, often called Revenue Stamps, at a rate of $2.00 per $1,000 of the sale price. For a $1.5 million estate in Blowing Rock, this amounts to a $3,000 charge typically paid by the seller, though negotiations in 2026 can shift this. You must also account for recording fees in Watauga or Avery County. Deeds currently cost $26 for the first 15 pages, while a Deed of Trust is $64 for the first 35 pages. Title insurance is another critical safeguard. New rates effective February 1, 2026, ensure your investment is protected against historical claims or boundary disputes, which are common in rugged mountain terrain.

Beyond these government mandates, you’ll need to prepay certain items to establish your escrow account. This includes a full year of homeowners insurance and pro-rated property taxes based on local rates, like Watauga County’s 0.43% or Ashe County’s 0.44%. If you’re purchasing within a gated community, HOA pro-rations and transfer fees will also appear. To ensure your budget accounts for every nuance of these land and acreage sales, consulting with a regional specialist is the best way to avoid surprises. Professional surveys and septic inspections are third-party costs that provide peace of mind before you sign the final deed.

The North Carolina Differentiator: Due Diligence vs. Earnest Money

North Carolina operates on a unique “Due Diligence” contract system that often catches out-of-state buyers by surprise. Unlike other regions where a single deposit sits in escrow, NC requires two distinct payments. These payments are central to your total closing costs in North Carolina. The first is the Due Diligence fee, a non-refundable amount paid directly to the seller. This fee buys you the right to walk away for any reason during a set period. The second is Earnest Money, which is held in escrow and remains refundable if you terminate the contract before the due diligence deadline. Understanding the balance between Due Diligence vs. Earnest Money is vital for protecting your capital while demonstrating serious intent to a seller.

Mastering the Due Diligence Fee

The Due Diligence fee is your “skin in the game.” While it’s credited toward the purchase price at settlement, you won’t get it back if you decide the mountain slope is too steep or the well yield is too low. In the competitive luxury markets of Banner Elk or Blowing Rock, these fees have become a primary negotiation tool. For a high-end estate, a larger fee can make your offer stand out in a sea of contingencies. Conversely, when purchasing raw land, the fee might be lower, but the timeline is often longer to accommodate perk tests and environmental surveys. This period is your window to uncover every detail of the property before your earnest money also becomes non-refundable.

The Essential Role of the NC Closing Attorney

North Carolina is an “attorney state,” meaning a licensed lawyer must oversee the closing process rather than a title company. This requirement adds a layer of legal protection that is invaluable for complex mountain transactions. Your attorney performs the title search, prepares the deed, and ensures all funds are disbursed correctly. Typical attorney fees for a standard closing range from $750 to $1,250, but luxury transactions often cost between $1,500 and $3,000 or more due to the complexity of estate titles and easement reviews. These professionals act as the final gatekeeper for your investment.

Lori Eastridge coordinates directly with local legal experts to ensure your settlement statement is accurate and all local nuances are addressed. During the due diligence period, your attorney’s title opinion is what allows you to move forward with confidence. If issues arise, such as undisclosed easements or boundary discrepancies, we use this time to negotiate seller credits. With 2026 trends showing that 47% of resale closings involve some form of seller concession, we can often leverage these findings to have the seller cover a portion of your final costs. This turns a potential deal-breaker into a strategic advantage before you ever reach the closing table.

Calculating Costs for High Country Estates and Mountain Land

Purchasing a home in the Blue Ridge Mountains involves more than just standard administrative fees. The rugged topography and elevation of our region introduce what locals often call the “Mountain Tax.” These are specialized inspections and logistical requirements that ensure your high-elevation investment is sound. While these items represent a small fraction of the overall closing costs in North Carolina, skipping them can lead to significant financial liabilities down the road. High Country buyers must account for these variables early to maintain a realistic budget for their legacy property.

Luxury Estate Inspection Variables

Luxury mountain estates require a more sophisticated vetting process than suburban residential properties. Radon testing is a standard but essential expense here, as the granite-rich soil of the Appalachians can produce higher levels of this gas. You should also budget for a structural engineer’s review if the home is built on a significant slope. These professionals verify that the foundation and retaining walls are managing the terrain’s natural drainage and pressure correctly. High-end properties often feature complex HVAC systems or whole-home generators that require their own specialized inspections. Don’t forget the CL-100 wood-infestation report; it’s a staple in our region to protect your timber-framed or log-accented home from local pests.

Acreage and Land Acquisition Costs

Buying land requires a different financial playbook. A precise boundary survey is your most important tool, especially when looking at unrestricted land for sale in Ashe County. Mountain property lines are notoriously complex, often relying on historical markers that have shifted over decades. You’ll also need to fund a soil evaluation, or perk test, to determine where a septic system can be installed. Without a passing perk test, your dream of building a mountain retreat could be stalled indefinitely. Well water testing for yield and quality is another non-negotiable land cost that ensures your future home has a reliable water source.

Exclusive mountain communities in areas like Banner Elk or Blowing Rock often charge HOA or POA transfer fees at closing. These can range from a few hundred to several thousand dollars depending on the community’s amenities. If your property borders the Blue Ridge Parkway, you may also need an elevation certificate to satisfy specific federal or local zoning requirements. Finally, always check for road maintenance agreements in your closing documents. If you’re on a private mountain road, you’ll likely be responsible for a pro-rated share of snow removal and grading costs. To find properties that meet your specific land-use goals, discover premier mountain estates with an expert who knows every ridge and valley of the High Country.

Navigating the Closing Table with Lori Eastridge

The journey to securing a mountain retreat culminates at the closing table, where abstract negotiations transform into a tangible legacy. In the High Country, this final stage requires more than just administrative oversight; it demands the advocacy of a localized expert who understands the nuances of luxury mountain transactions. Precision is our priority. We don’t just facilitate a signature. We ensure that every detail, from the structural integrity of a hillside foundation to the clarity of a deed in Watauga County, aligns with your long-term goals. By identifying potential deal-breakers during the due diligence period, we protect your capital and your peace of mind before you ever commit to the final closing costs in North Carolina.

Before you reach the attorney’s office, a strategic final walkthrough is essential. This isn’t a mere formality for a mountain estate. We verify that specialized systems, such as whole-home generators and high-yield well pumps, are functioning as promised. We also ensure that the property’s condition hasn’t shifted since the initial inspections. This meticulous attention to detail ensures that your transition from buyer to owner is seamless and that your new home is truly move-in ready the moment the keys are handed over.

Strategic Negotiation and Advocacy

Our role as your strategic partner involves rigorous scrutiny of the Closing Disclosure (CD). We review every line item for accuracy, ensuring that lender fees and pro-rated taxes are calculated correctly. Leveraging current market data from our NC Real Estate Investment guide, we provide the justification needed for fair pricing and favorable terms. In early 2026, approximately 47% of resale closings in competitive North Carolina regions included seller concessions. We utilize this trend to negotiate credits that can offset your initial investment, turning the complexities of closing costs in North Carolina into a managed component of your financial strategy.

Your High Country Lifestyle Begins

On closing day, you’ll meet with a licensed North Carolina attorney to finalize the transfer of your deed. You’ll need to bring a valid government-issued ID and ensure that your certified funds or wire transfers are prepared according to the attorney’s specific instructions. Once the deed is recorded at the county courthouse, the property is officially yours. Our commitment to your success doesn’t end when the paperwork is filed. We provide bespoke post-closing support, connecting you with the region’s most reliable vendors and service providers to help you settle into the Blue Ridge community with ease.

Ready to secure your place in the mountains? Schedule a consultation with Lori Eastridge to start your search and experience a higher level of real estate service tailored to the High Country lifestyle.

Securing Your High Country Legacy

Mastering the final steps of your property acquisition ensures that your transition into mountain living is as serene as the views from your new deck. You now have the tools to differentiate between non-refundable due diligence fees and earnest money, while accounting for the specialized inspections essential for high-elevation terrain. By anticipating these specific line items, you can approach the settlement table with absolute financial clarity. Navigating closing costs in North Carolina requires a partner who understands that these transactions are about more than just numbers; they’re about protecting your future in the Blue Ridge.

Lori Eastridge provides this elite level of advocacy, bringing over 7 years of High Country expertise and specialized Luxury Estate and Land certifications to every deal. Our personalized brokerage, powered by eXp Realty, combines global reach with the intimate knowledge of a local insider. We’re dedicated to transparency and meticulous detail, ensuring your investment is sound from the first tour to the final signature. Your mountain retreat is within reach, and we’re here to lead the way with confidence and regional warmth.

Explore Luxury Mountain Estates with Lori Eastridge

Frequently Asked Questions

What is the average percentage for closing costs in North Carolina for 2026?

Buyers should budget between 2% and 5% of the total purchase price for their closing costs in North Carolina. For a home priced at the 2025 median of $382,211, this typically amounts to a range of $7,600 to $19,100. These figures cover lender fees, government taxes, and prepaid items. In the High Country, luxury transactions often lean toward the higher end of this range due to more extensive due diligence requirements.

Who typically pays for the title insurance in a North Carolina transaction?

The buyer typically pays for title insurance in North Carolina, though it remains a negotiable item during the offer phase. New rates effective February 1, 2026, ensure these costs are regulated by the state’s Department of Insurance. This one-time premium protects your mountain investment from historical title defects or boundary disputes. For luxury estates with complex deed histories, this coverage is a non-negotiable safeguard for your equity and peace of mind.

Is the Due Diligence fee separate from the closing costs?

The due diligence fee is paid upfront to the seller but is credited back to you as a line item on your settlement statement. While it’s technically part of your total out-of-pocket investment, it’s handled differently than other closing costs in North Carolina. It’s non-refundable if you walk away. However, it effectively reduces the amount of cash you need to bring to the table on your final closing day.

Does North Carolina require a lawyer to be present at the real estate closing?

North Carolina law requires a licensed real estate attorney to oversee the closing process and the disbursement of funds. This ensures that the title search is conducted properly and that all legal documents are recorded accurately in counties like Watauga or Ashe. Your attorney acts as a vital neutral party who coordinates with your lender and broker. This legal oversight provides an essential layer of security for high-stakes mountain transactions.

Can I include my closing costs in my mortgage loan?

Most conventional lenders don’t allow you to roll closing costs directly into your mortgage loan. However, you can negotiate seller concessions to offset these expenses. In early 2026, nearly 47% of resale closings in the state included such concessions. This strategy allows you to keep more liquid capital available for immediate mountain lifestyle upgrades or land improvements after you’ve secured your new property and moved into the High Country.

How much should I budget for a land survey in the High Country?

Budgeting for a land survey depends heavily on the acreage and the complexity of the mountain terrain. While we don’t quote specific pricing for these third-party services, expect higher costs for large, wooded parcels with significant elevation changes. A precise boundary survey is critical in the High Country to identify encroachments or easement issues. We always recommend getting a firm estimate from a local surveyor early in your due diligence period.

What happens to my Earnest Money if the deal falls through during Due Diligence?

Your earnest money is generally refunded if you terminate the contract before the due diligence period expires. This deposit is held in a trust account as a sign of good faith. Unlike the non-refundable due diligence fee, the earnest money remains protected until the deadline passes. If you decide to walk away after the due diligence date, you’ll likely forfeit this deposit to the seller as liquidated damages for taking the home off the market.

Are closing costs higher for luxury homes in Blowing Rock or Boone?

Total dollar amounts for closing costs are naturally higher for luxury estates in Blowing Rock or Boone, even if the percentages remain consistent. High-end homes often require more expensive, specialized inspections for structural integrity on steep slopes or complex HVAC systems. Additionally, attorney fees for luxury closings can range from $1,500 to over $3,000. This reflects the increased time required to review intricate estate titles and community-specific HOA regulations common in our region.

{kind=link}